Uniform Guidance

Uniform Administrative Requirements, Cost Principles, and Audit Requirements

To deliver on the promise of a 21st-Century government that is more efficient, effective and transparent, the Office of Management and Budget (OMB) is streamlining the Federal government's guidance on Administrative Requirements, Cost Principles, and Audit Requirements for Federal awards.

COFAR was created in 2011 and took over the lead in crafting the OMB Uniform Guidance (UG) and continues to lead efforts to improve policies and practices related to federal grants and cooperative agreements. The UG will supersede requirements from eight OMB Circulars:

- A-21 Principles for Determining Costs Applicable to Grants, Contracts, and Other Agreements with Educational Institutions

- A-50 Audit Follow-Up

- A-87 Cost Principles for State, Local, and Indian Tribal Governments

- A-89 Federal Domestic Assistance Program Information

- A-102 Grants and Cooperative Agreements with State and Local Governments (Administrative Procedures)

- A-110 Uniform Administrative Requirements for Grants and Other Agreements with Institutions of Higher Education, Hospitals, and Other Nonprofit Organizations

- A-122 Cost Principles for Nonprofit Organizations

- A-133 Audits of States, Local Governments, and Nonprofit Organizations (2009 Compliance Supplement and Addendum)

Institutional Impact and Implementation

Institutions of Higher Education (IHEs) - typically subject to A-21, A-110, and A-133 - are determining how best to transition to the new guidance.

Until promulgated by federal agencies in their grant guidelines and award documents, there are few clear implementation strategies.

What we know:

- The Uniform Guidance applies to new awards and incremental funding obligated on or after December 26, 2014.

- Subpart F, Audit Requirements will be effective for the first fiscal year following 12/26/2014 (e.g. July 1, 2015–June 30, 2016).

- Implementation of the Procurement Standards has been delayed until the end of the first fiscal year following 12/26/2014 (e.g. July 1, 2016) - see COFAR FAQ (11/26/2014) 200.110-6

- Projects awarded prior to December 26, 2014, will be managed under the terms and conditions included with the original award (A-21, A-110, A-133, agency provisions, award terms) unless formally modified via a separate modification or as part of next incremental award.

- There is still some ambiguity about required approvals and “expanded authorities.”

What appear to be the most significant changes:

In general:

- Increased requirements for prior approval (2 CFR 200.407)

- Increased focus on performance evaluation (2 CFR 200.301)

- Increased emphasis on internal controls (2 CFR 200.303)

In particular:

- Cost Sharing (2 CFR 200.306)

- Voluntary committed cost share is not expected and cannot be used as a merit review factor for proposals or applications unless specified in the notice of funding opportunity or detailed in agency regulations

- See ORSP's guide to Sponsored Program Cost Sharing

- Direct Charging of Administrative and Clerical Salaries if all required criteria met and documented (2 CFR 400.413 (c))

- See ORSP's guide to Proposal Budget Information

- Direct Charging of Computer Devices (2 CFR 200.453) when documented

- See ORSP's guide to Computers & Electronic Devices

- Personal Compensation, especially Effort Reporting (2 CFR 200.430)

- Emphasis on institutional internal controls

- No change in effort reporting at UM

- Preparing, Issuing, and Monitoring Subawards and Subcontracts (2 CFR 200.330, 331, 332)

- Emphasis on institutional internal controls in making determination between contracted services/vendor and subrecipient 2 CFR 200.330 (c)

- See UM's guide to Subrecipient Agreements

- If subrecipient does not have a federally-negotiated rate, a 10% MTDC de minimis rate may be recovered. (2 CFR 200.331.(a).4)

- Emphasis on institutional internal controls in making determination between contracted services/vendor and subrecipient 2 CFR 200.330 (c)

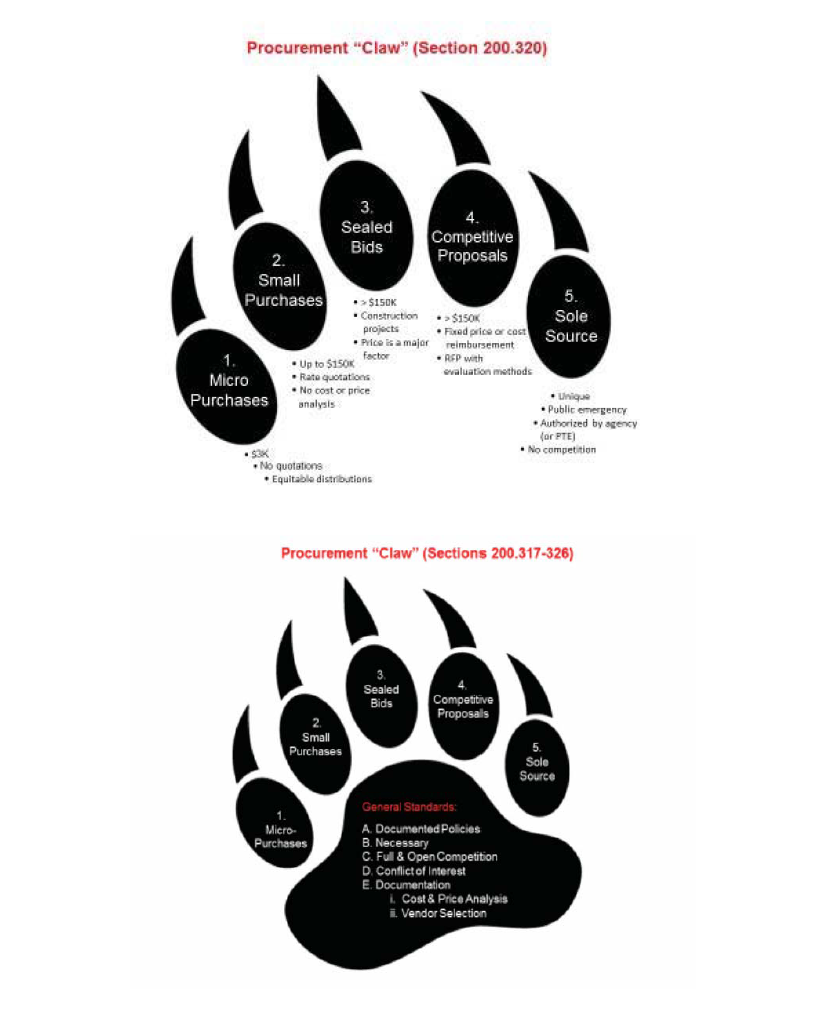

- Procurement Requirements

- Per COFAR FAQ (11/26/2014) 200.110-6, UM will continue to comply with OMB Circular A-110 until July 1, 2016

- Per COFAR FAQ (11/26/2014) 200.110-6, UM will continue to comply with OMB Circular A-110 until July 1, 2016

References

2 CFR 200 - Uniform Guidance

Council on Financial Assistance Reform (COFAR) (See FAQ’s, 11/26/2014)

COFAR Webcast on Uniform Guidance Implementation (five parts)

Council on Governmental Relations (COGR) (See Guide to the Uniform Guidance, Version 2, 09/17/2014)

Office of Management and Budget (OMB) Policy Statement - Uniform Grant Guidance

Comparison charts:

- Uniform Guidance Crosswalk from Existing Guidance to Final Guidance

- Uniform Guidance Crosswalk from Final Guidance to Existing Guidance

- Cost Principles Comparison Chart

- Audit Requirements Comparison Chart

- Administrative Requirements Comparison Chart